The economic impact of climate change has become a central concern for policymakers and economists alike, as projections now indicate that the financial consequences could be far more severe than previously estimated. A recent study highlights that for every additional 1°C increase in global temperatures, we could see a staggering 12 percent drop in global GDP. This alarming figure underscores the critical nature of addressing the climate change economy, revealing the potential for widespread economic disruption. Furthermore, the social cost of carbon is also much higher than past calculations, reinforcing the argument for immediate and effective decarbonization strategies. As we face unprecedented weather events and shifts in productivity, understanding the economic toll of climate change will be essential for crafting policies that ensure a sustainable and profitable future.

Exploring the financial ramifications of environmental shifts, we delve into the significant consequences of global warming on markets and economies. As climate conditions worsen, the overall impacts on gross domestic product (GDP) and economic resilience come into sharper focus. The implications of rising temperatures not only threaten to disrupt various economic sectors but also highlight the urgent need for innovative decarbonization strategies. Assessing the social costs associated with carbon emissions becomes pivotal in calculating the long-term benefits of transitioning to greener technologies. Ultimately, addressing the repercussions of climate change on the economy necessitates a comprehensive understanding of its far-reaching consequences.

Understanding the Economic Impact of Climate Change

The economic impact of climate change is becoming increasingly evident as global temperatures continue to rise. Recent studies suggest that each incremental increase in temperature brings significant reductions in gross domestic product (GDP), with estimates indicating losses of up to 12 percent for every additional degree Celsius. This alarming statistic underscores the need for urgent action: ignoring climatic shifts could lead to dire economic consequences that outstrip previous modest projections.

Moreover, the economic toll of climate change extends beyond immediate GDP losses. It encapsulates long-lasting damage to productivity, increased costs from extreme weather events, and the social cost of carbon emissions. As scientists warn, the correlation between rising global temperatures and heightened frequency of severe weather events means that the long-term economic forecasts may still underestimate future risks. Therefore, re-evaluating macroeconomic models to incorporate these factors has never been more critical.

The Relationship Between Climate Change and GDP

The relationship between climate change and GDP is a complex interplay that requires careful examination. Historically, economists have often underestimated the adverse effects of climate change on productivity and overall economic performance. A new approach focusing on global temperature rather than local temperature fluctuations has revealed that every 1°C rise could lead to a staggering 12 percent decline in GDP. This understanding necessitates rigorous evaluations of past economic models, which typically failed to account for the escalating dangers posed by climate variations.

As countries struggle to adapt to warming conditions, the implications for GDP become even more critical. The continuous nature of economic growth, driven by factors like technological advancement, may mask the severe losses incurred from climate-related disruptions. For instance, while growth rates might suggest economic stability, the reality is more nuanced; ongoing climate change could mean that future prosperity is significantly curtailed compared to what could have been achieved in a stable climate.

The Social Cost of Carbon: Rethinking Economic Models

The social cost of carbon (SCC) is an essential metric for understanding the economic ramifications of greenhouse gas emissions. Recent research suggests that the SCC has been undervalued in previous assessments, often leading to an incomplete picture of the costs associated with climate change. In their findings, Bilal and Känzig estimate the SCC at $1,056 per ton globally, an eye-opening revelation compared to earlier estimates of merely $185 per ton. Such discrepancies highlight the necessity of incorporating comprehensive economic data into climate policies.

This recalculated social cost also has direct implications for national decarbonization strategies. When the SCC reflects the true costs of carbon emissions, it is easier to justify investments in green technologies and renewable energy. For instance, the cost of federal decarbonization interventions, as indicated by the 2022 Inflation Reduction Act, is significantly lower at approximately $95 per ton. Consequently, this shows that the economic rationale for transitioning to a sustainable economy is not only beneficial but imperative in mitigating climate change effects.

Decarbonization Benefits: Economic Arguments for Sustainability

The case for decarbonization transcends environmental necessity; it presents a compelling economic opportunity. By implementing stringent climate policies, countries can not only reduce their carbon footprint but also stimulate economic growth through job creation in renewable energy sectors. The recent analysis indicates that decarbonization can easily pass a cost-benefit analysis for major economies such as the U.S. and the European Union, reinforcing the idea that proactive climate action is not only ecologically sound but economically profitable.

Furthermore, as nations embark on the journey toward a low-carbon economy, the benefits become increasingly multifaceted. Initiatives like investments in clean energy infrastructure lead to enhanced energy security, reduced healthcare costs from improved air quality, and resilient job markets that can withstand the shocks of climate change. The transition to a sustainable economy is thus not just a moral imperative but a strategic economic move that can safeguard future prosperity against the uncertainties of climate-induced risks.

The Role of Technological Innovation in Addressing Climate Change

Technological innovation plays a crucial role in addressing the challenges posed by climate change. As the global community faces the adverse effects of rising temperatures, advancements in clean energy technologies offer viable solutions to mitigate climate impacts. Innovations such as solar energy, wind power, and energy storage systems are central to the decarbonization movement, presenting significant economic opportunities while reducing dependence on fossil fuels. Moreover, these technologies can enhance productivity and stabilize job markets that may otherwise suffer from climate-linked disruptions.

Furthermore, the integration of new technologies not only helps reduce emissions but also has the potential to lead to GDP growth through increased efficiency and decreased external costs associated with climate change. As firms invest in greener technologies, they position themselves competitively in a market increasingly driven by sustainability goals, thus creating a positive feedback loop that benefits both the economy and the environment. In this way, technological innovation acts as a cornerstone for achieving a resilient future amidst the challenges of climate change.

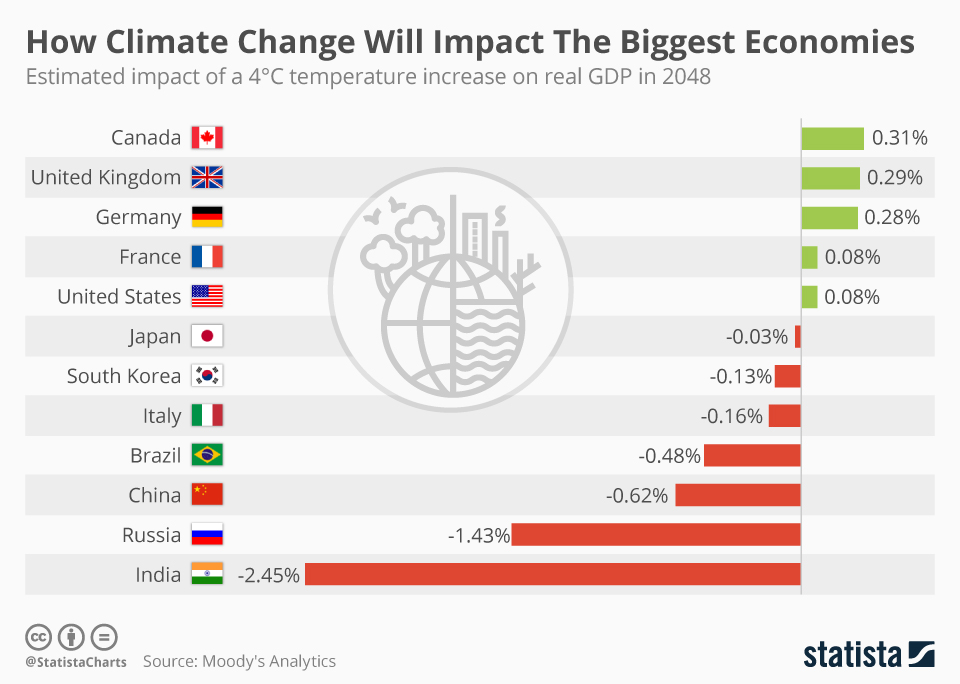

The Global Perspective: Climate Change Economics Around the World

Understanding the economic impact of climate change requires a global perspective. Different regions experience varying consequences, shaped by their geography, level of industrialization, and adaptive capacities. For instance, developing nations often bear the brunt of climate change effects, affecting agricultural productivity and leading to increased food insecurity. In contrast, industrialized nations are grappling with the economic toll from severe weather events, infrastructure damage, and higher adaptation costs. This divergence emphasizes the necessity for collaborative international efforts to address these challenges.

It is also vital to recognize the interconnectedness of global economies when discussing climate change projections. The effects of climate change in one part of the world can ripple through trade networks, impacting GDP in diverse regions. Therefore, global cooperation in climate finance and technology transfer is crucial for fostering resilience and minimizing economic fallout. By sharing knowledge and resources, countries can mitigate the impacts of climate change more effectively and ensure a more equitable distribution of the economic burdens and benefits associated with climate action.

Future Projections: Economic Consequences of Inaction

Future projections regarding the economic consequences of inaction on climate change are increasingly dire. Research suggests that without significant interventions, global output and consumption may face irreversible declines, with estimates indicating a potential 50 percent reduction by 2100. Such staggering losses indicate not only the urgency of addressing climate change but also the profound implications for economic stability across the globe. The longer actionable measures are delayed, the more catastrophic the outcomes will be for GDP and overall economic health.

Moreover, inaction will likely exacerbate existing inequalities as vulnerable populations and economies suffer disproportionately from climate-related impacts. Areas already facing economic challenges may find themselves locked in a downward spiral, further limiting their capacity to recover or adapt. Thus, immediate action is required not only to prevent severe economic repercussions but also to support those most affected by climate change. Investing in sustainable practices and climate resilience is crucial in averting unmanageable economic distress in the future.

The Interconnection Between Economic Growth and Environmental Health

The interconnection between economic growth and environmental health cannot be overstated in the context of climate change. Historically, economic development has often been pursued at the cost of environmental integrity, leading to unsustainable practices and long-term ramifications. As recognition grows regarding the importance of environmental stewardship, policymakers are increasingly realizing that a healthy economy cannot be separated from a healthy planet. Sustainable growth strategies that prioritize environmental health are becoming essential in ensuring future economic viability.

These sustainable development strategies include promoting green technologies, improving energy efficiency, and implementing policies that encourage responsible resource management. By aligning economic objectives with environmental health, governments can create pathways that lead to mutual benefits. In this way, fostering an economy that respects ecological balances not only protects our planet but also enhances economic resilience against the adverse effects of climate change. The integration of sustainability into core economic practices is a pivotal step toward securing a stable and prosperous future.

Strategies for Mitigating the Economic Effects of Climate Change

Mitigating the economic effects of climate change requires a multifaceted approach that combines innovative strategies with cohesive policies. Governments and businesses must collaborate to develop comprehensive climate action plans that lower emissions while promoting economic growth. Key strategies can include investments in renewable energy, incentivizing green innovation, and enhancing public transportation systems to reduce reliance on fossil fuels. These measures not only demonstrate a commitment to mitigating climate risks but also generate employment and stimulate economic activity.

Additionally, adapting to the already-inevitable impacts of climate change necessitates strategic financial planning. Allocating resources for climate resilience and adaptation infrastructure—such as flood defenses and drought-resistant agriculture—will be essential for safeguarding economies. By prioritizing strategic investments that address both climate change and economic stability, nations can create a robust framework that protects future generations from the compounding economic toll of inaction.

Frequently Asked Questions

What is the economic impact of climate change on global GDP?

Recent studies indicate that the economic impact of climate change could lead to a 12 percent reduction in global GDP for every additional 1°C rise in temperature. This prediction suggests that the economic toll of climate change is significantly larger than previous estimates, with potential losses peaking shortly after the temperature increases.

How does climate change affect productivity and the economy?

Climate change negatively impacts productivity by increasing the frequency and severity of extreme weather events, which can disrupt economic activities. The new estimates suggest that as global temperatures rise, the economy faces diminishing returns, leading to a substantial economic toll on various sectors.

What is the social cost of carbon and why is it important for understanding the climate change economy?

The social cost of carbon represents the economic cost associated with emitting one additional ton of carbon dioxide. A recent recalculation estimated this cost at $1,056 per ton globally. Understanding this figure is crucial, as it informs policy decisions related to climate change and the economic benefits of decarbonization measures.

What are the decarbonization benefits outlined in recent economic studies?

Decarbonization benefits include substantial economic gains, as newer studies demonstrate that the costs of implementing decarbonization policies—such as those covered by the Inflation Reduction Act—are outweighed by the long-term savings from avoiding the severe economic toll of climate change.

How do extreme weather events relate to the economic impact of climate change?

Extreme weather events are becoming more frequent due to climate change and have severe implications for the economy. These events can damage infrastructure, reduce productivity, and lead to increased costs, highlighting the urgent need to address the economic impact of climate change through effective policies.

Why is there a disconnect between climate scientists and macroeconomists regarding climate change forecasts?

Historically, climate scientists have presented dire warnings about the impacts of temperature increase, while macroeconomists have often predicted more moderate effects. Recent research aims to bridge this gap by emphasizing that the economic impact of climate change will be more severe than previously believed.

What countries are projected to suffer the most economic impact due to climate change?

Economic projections estimate that climate change will affect countries differently, with the modeling conducted in recent studies covering 173 countries. The effects will depend heavily on regional vulnerability to temperature increases and extreme weather, underscoring the broader implications of climate change on global economic stability.

| Key Point | Details |

|---|---|

| Economic Forecast | New study reveals that the economic toll of climate change is projected to be six times larger than prior estimates, indicating serious implications for global GDP. |

| Global Temperature Impact | Each additional 1°C rise in global temperature is linked to a 12% decrease in global GDP, with maximum loss occurring six years after the temperature rise. |

| Historical Comparison | A hypothetical increase of 2°C by 2100 could lead to a 50% reduction in output, significantly surpassing the economic effects of the Great Depression. |

| Decarbonization Policy | The study suggests that global decarbonization efforts are economically viable, passing the cost-benefit analysis for major economies. |

Summary

The economic impact of climate change is profound and alarming, as new research reveals that the costs are much higher than previously estimated. With each degree of temperature rise inflicting a significant decline in global GDP, the urgent need for effective climate action becomes unmistakable. Addressing climate change is not only crucial for environmental stability but also essential for sustaining economic growth, making decarbonization efforts not just necessary but economically beneficial.